Santa Claus’s gift to the bond markets last week was some relevant economic numbers after weeks of “old” numbers that were backed up since the government shutdown started on October 1st (and ended on November 12th when Congress passed a funding bill that was signed into law by the President).

Last week we had the following (a few samples).

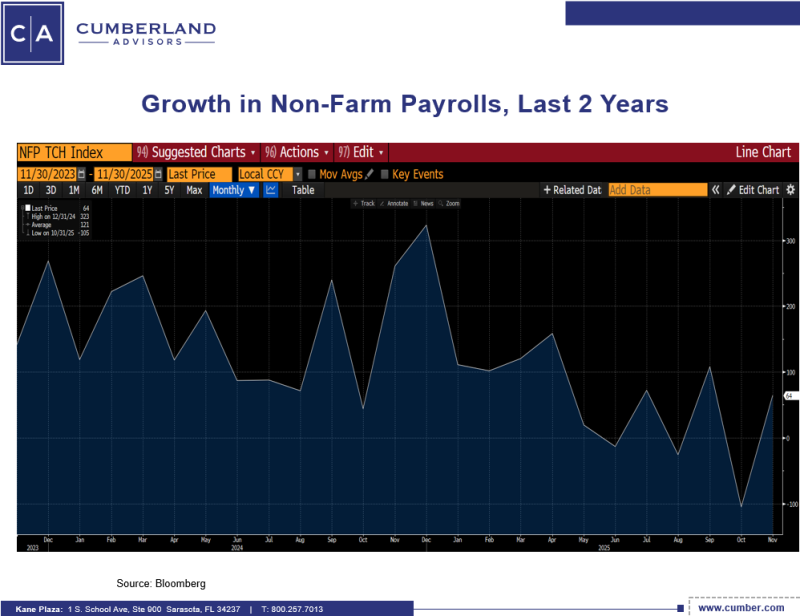

Change in non-farm payrolls, November:

Expectation, 50k – actual, 64k (prior month -105k)

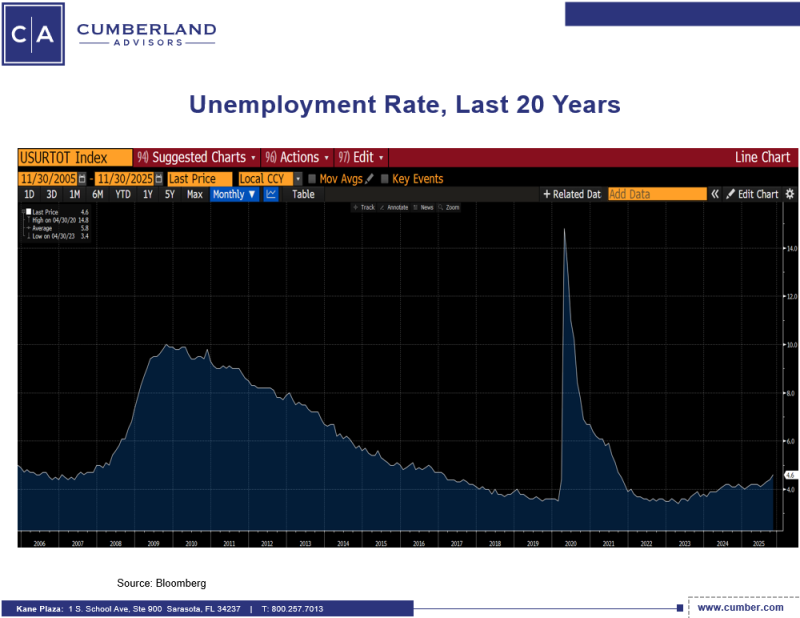

U3 unemployment rate, November:

Expectation, 4.5% – actual, 4.6%

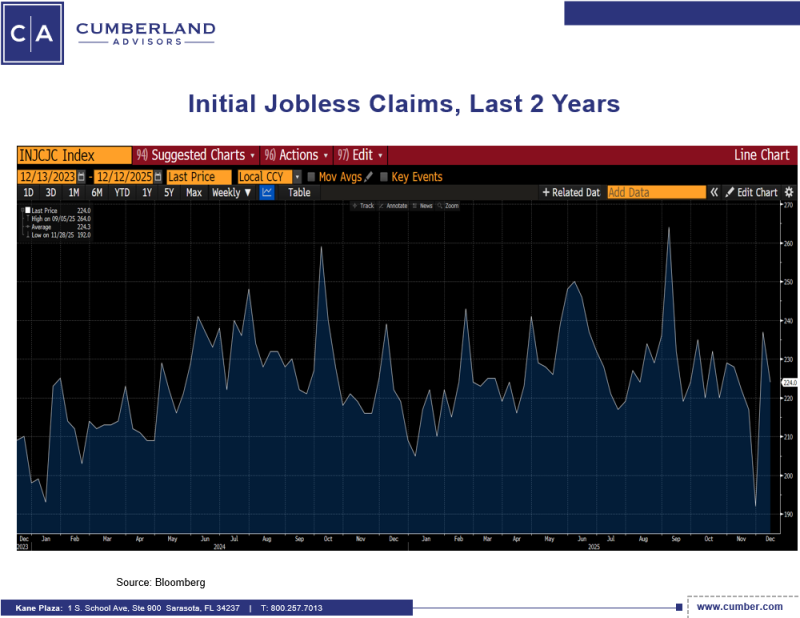

Initial jobless claims, week of Dec 13th:.

Expectation, 225k – actual, 224k

CPI year over year, November:

Expectation, 3.1% – actual, 2.7%

Looking at these, we can make the following observations.

Job creation is clearly declining. Part of that is related to the significant reduction in immigration under this administration. With fewer people, there is less NEED for jobs, and it shows in the numbers. The unemployment rate is certainly at the lower end compared to the past twenty years but has risen sharply since the end of last year, when it was 3.7% to the current 4.6%. It is this turn-up which has had the Fed shifting in balancing priorities between inflation and the labor markets. Last week saw the markets start to factor in two rate cuts or possibly more next year.

Initial jobless claims at 224k are really the average for the past two years. This sums up what David Berson, our Chief Economist, has been saying. We are in a “slow to hire but slow to fire” economy.

CPI year over year has not really made headway towards the 2% goal of the Fed, but it has not gone markedly above 3% either. The downward movement in year-over-year CPI is without the benefit of shelter numbers for November, but we know nationally that rents have started to drop. We will continue to watch this.

When we look at the comparison between trailing CPI and the ten-year US Treasury yield, we see a decline in both. It is important to remember that last January the ten-year US Treasury yield was at 4.8%, just before the Presidential inauguration. At that point, the fact that the President and both houses of Congress were on the same side was weighing heavily on the bond market. As it turned out, “Fear of Trump,” which had sent bond yields markedly higher since the beginning of the fall in 2024, was worse than Trump. That being said, the 30-year Treasury bond yield is 3 basis points higher than at the beginning of the year, while the 2-year Treasury bond yield is 74 basis points lower. The yield curve has definitely steepened.

Intermediate to longer bond yields still provide decently high coupon income.

We will continue to watch the numbers as we head into 2026. There are a number of cross currents. Higher delinquencies in credit cards and student loans and climbing unemployment are concerns. On the other hand, the new year will bring some stimulus in the form of tips not being taxed (up to a point). That will be stimulating at the margin. In addition, for the 2026 tax year, the state and local tax (SALT) deduction cap has been significantly raised above the old $10,000 limit to just above $40,000 for most taxpayers. That should provide extra cash flow at the margin as well. On full balance, we feel the economy is slowing but at a slow rate, with the upper part of the “K-shaped economy” carrying the ball.

We hope everyone on our subscriber list enjoys a healthy and happy end of the year holiday season. See you in 2026.

John R. Mousseau, CFA

Vice Chairman | Chief Investment Officer

Feedback | Bio

Sign up for our Market Commentaries

Cumberland Advisors Market Commentaries offer insights and analysis on upcoming, important economic issues that potentially impact global financial markets. Our team shares their thinking on global economic developments, market news and other factors that often influence investment opportunities and strategies.

Links to other websites or electronic media controlled or offered by Third-Parties (non-affiliates of Cumberland Advisors) are provided only as a reference and courtesy to our users. Cumberland Advisors has no control over such websites, does not recommend or endorse any opinions, ideas, products, information, or content of such sites, and makes no warranties as to the accuracy, completeness, reliability or suitability of their content. Cumberland Advisors hereby disclaims liability for any information, materials, products or services posted or offered at any of the Third-Party websites. The Third-Party may have a privacy and/or security policy different from that of Cumberland Advisors. Therefore, please refer to the specific privacy and security policies of the Third-Party when accessing their websites.