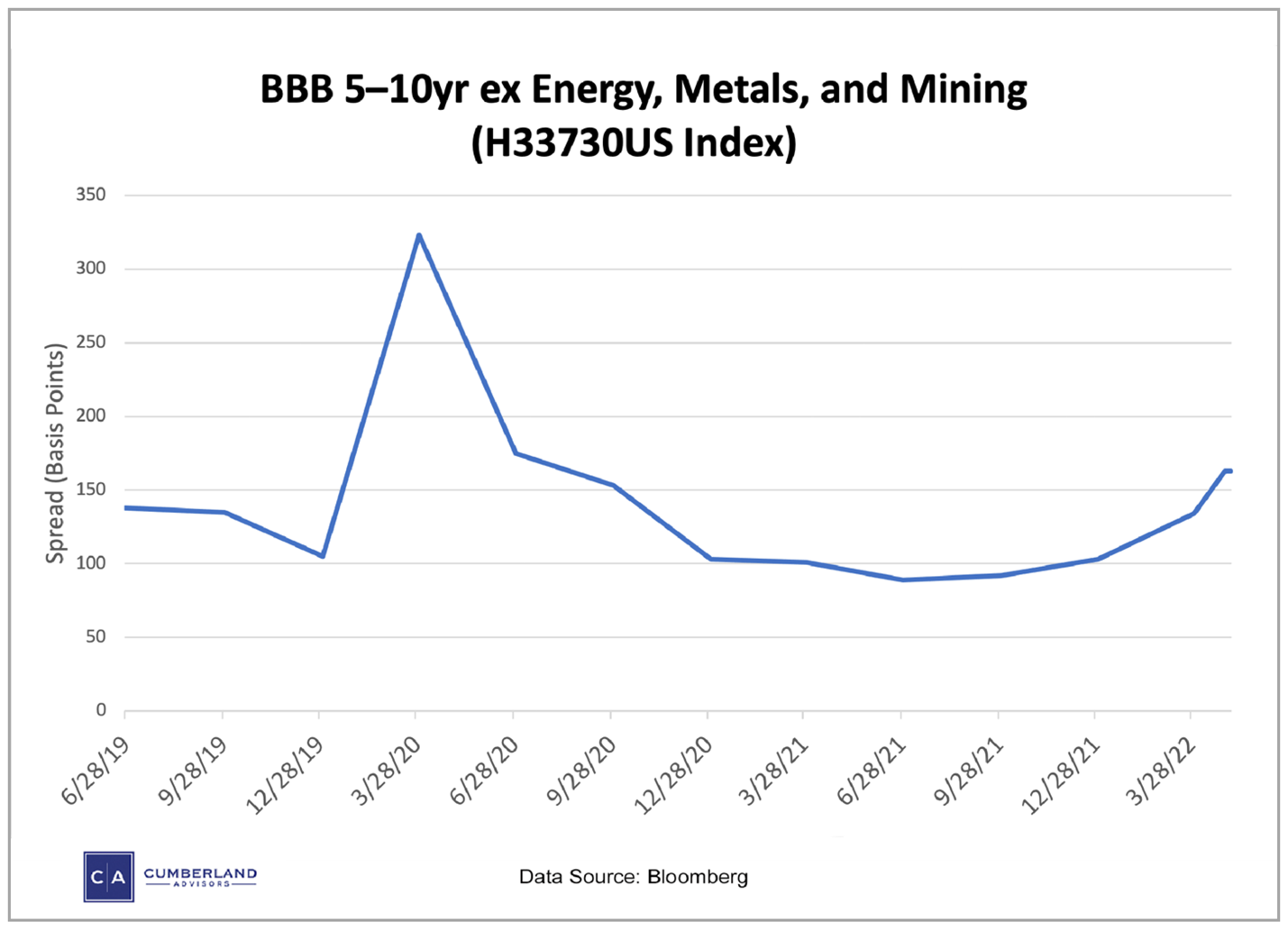

Today we are going to look at the credit spread of a Bloomberg intermediate-term BBB-rated bond cohort which is determined and priced AFTER removing the bonds of energy, metals, and mining. The series from Bloomberg is “BBB 5–10yr ex Energy, Metals, and Mining (H33730US Index).”

Why this series?

1. It shows us the lower level of investment-grade corporate bonds compared to riskless US Treasury notes of similar maturity. Thus it gives us the market-based pricing of the credit-spread differential.

2. By excluding the energy, metals, and mining sector debt, we are eliminating the effects of the high pricing that is bolstering those sectors. Remember that the bonds in those sectors were issued when prices in energy, metals, and mining were much lower than they are in the present market. So the bond’s creditworthiness has improved, because the companies issuing that debt are getting paid a higher price for their production than anticipated when the bonds were originally issued. We want to exclude this “windfall” improvement in credit so we can get a clearer picture of the creditworthiness of the rest of the bonds in the BBB rating arena.

3. The rest of this bond cohort is related to ongoing business credit risk in the United States. All these are US dollar-denominated bonds that trade in the American bond markets. The rising credit spread indicates market agents’ perception that the risk (and thus market-based pricing of this risk) is rising. Note that this is pure market pricing, so it doesn’t tell us why the price is changing. It is just the pricing itself. Interpretation is left to the analyst.

4. This measure of risk has widened out after a great narrowing during the post-Covid shock period. The chart below shows the movement of this spread. Note that the spread is higher now than it was before the Covid shock hit at the beginning of 2020.

5. The other aspect of this credit spread is that it is based on the intermediate portion of the yield curve, not the longer-term portion. So we don’t have the influence of the very-long-term maturities in the bond market.

6. The interpretation is that in the sectors depending on debt and NOT in the energy or metals business, credit risk is rising, and that rising risk is becoming apparent in the stock market when we look at indices like the Russell 2000. Remember that credit spreads correspond with stock price movements of the sectors that are affected in the debt markets. Also remember that this level of BBB credit rating more closely corresponds with the credit levels of most companies. Very few companies are truly AAA-rated credits.

7. The level of this credit spread is a warning. If it doesn’t widen more, we can expect a “soft landing” coming, and this market-based pricing will reflect that outlook. If it does widen further, we would see that as a “flashing yellow light” taking us in the wrong direction.

Meanwhile, our US Equity ETF portfolio is maintaining a cash reserve.

Here’s the chart.

David R. Kotok

Chairman & Chief Investment Officer

Email | Bio

Links to other websites or electronic media controlled or offered by Third-Parties (non-affiliates of Cumberland Advisors) are provided only as a reference and courtesy to our users. Cumberland Advisors has no control over such websites, does not recommend or endorse any opinions, ideas, products, information, or content of such sites, and makes no warranties as to the accuracy, completeness, reliability or suitability of their content. Cumberland Advisors hereby disclaims liability for any information, materials, products or services posted or offered at any of the Third-Party websites. The Third-Party may have a privacy and/or security policy different from that of Cumberland Advisors. Therefore, please refer to the specific privacy and security policies of the Third-Party when accessing their websites.

Cumberland Advisors Market Commentaries offer insights and analysis on upcoming, important economic issues that potentially impact global financial markets. Our team shares their thinking on global economic developments, market news and other factors that often influence investment opportunities and strategies.