This may be the quarter that muni credit quality begins to turn. However, munis are an extremely safe asset class and often viewed as a flight to quality product. There have been many more upgrades than downgrades over the past few years, so one might expect the trend to plateau; and then, of course, there are the challenges ahead. They include demographic changes such as our aging population; changes in the federal approach to healthcare, education, disaster relief, immigration, and tariffs; as well as the response of the economy or pockets of the economy to the changes. Other challenges include protecting against increasing cyberattacks as well as natural disasters and extreme climate events – and increasing insurance costs for these hazards. Munis with the strongest credit quality in the AA category and above should show resiliency in facing these challenges even with a turn of credit.

The Fed lowered short-term interest rates in September, with the slowdown in job growth and mixed inflation readings to hang their hat on. Most market participants at this juncture anticipate further rate cuts in October and December. The federal government shutdown and lack of agreement on a budget generate further uncertainty for munis to manage, and regions with more than average federal employment may experience greater job losses. DC, Maryland and Prince Georges County, MD, have already experienced downgrades, partly because of exposure of their economies to the pullback in federal employment.

We expect increases in leverage as munis issue more debt to improve aging infrastructure and resiliency, and to retain funds to keep reserves bolstered rather than using excess revenue for capital expenditures. The lowering of interest rates will generally make financing and refinancing less costly. There is capacity for debt to be issued, because many municipalities deferred raising debt over the past few years. However, additional debt will increase leverage and could reduce financial cushions without the managing of expenses or raising of rates and/or taxes to service the debt.

In August Moody’s released rating activity showing that over Q2 downgrades surpassed upgrades – a definite change in trend. However, several of the downgrades were related to Moody’s downgrade of the US; and filtering them out, the ratio of upgrades to downgrades was positive but did narrow. See our commentary “Moody’s Downgrade of the US to Aa1 and the Ripple Effect on Bond Ratings.”

Despite the moderating of the ratio of upgrades to downgrades, five states had positive rating adjustments over Q3: Maine, New Jersey, Connecticut, Alaska and Wyoming. See our state section towards the end of this commentary. Meanwhile, Pennsylvania is months past its budget deadline; and while the state credit has become more robust (current ratings are A+ positive outlook by S&P, Moody’s Aa2 and Fitch AA), as the impasse continues it may put strain on localities, causing them to conduct budgetary cuts or short-term borrowing. This is a mark on the state’s governance – just like it was for the downgrade of the United States – and if it continues, there could be a negative rating action on the state or localities within the state. We generally include information on state rating changes in our credit commentary because state fiscal health can have ramifications for funding decisions at the local level. The actions that states take after some of the potential federal changes are more clearly known will be closely watched by taxpayers and market participants.

Many municipalities have received upgrades for having better-funded reserves, which can indicate better budgeting and/or growth in population or economic activity. Improved pension funding is another item that has contributed to rating upgrades. S&P released a report in August that discussed rising pension funding levels due to improved investment returns. The accumulation of reserves and continued pension funding are tempting for a muni to reduce in times of economic strain and are a sign of concern to analysts and rating agencies when they are not adequately addressed.

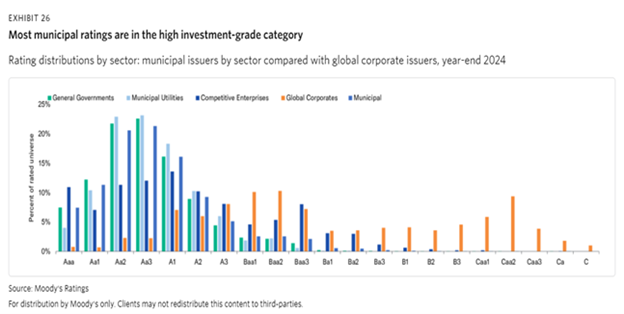

Most rated muni bonds have very good credit quality. Outstanding municipal bonds total about $4 trillion; and there are 90,000 municipal issuers as of the last census of governments in 2022, ranging in size from a park district to a large urban city to a special-purpose entity. In the chart below you can see that corporate bonds skew to the BBB range while muni bonds skew to AA. Corporate credit quality has also been on a positive trend. JPMorgan compiled corporate ratings changes in an Oct 6th report. The year-to-date upgrade/downgrade ratio stands at 1.9x. This is a lower ratio but has been positive since 2021. The upgrade/downgrade ratio was 4.7x in 2024, 3.5x in 2023, 3.9x in 2022 and 1.1x in 2021. About $1.8tr of debt has been net upgraded since 2021. Corporate spreads over the comparable Treasury rate – an indicator of perceived credit risk – has been tight, indicating low perceived risk.

State Rating Changes

Maine upgraded to AA+ by Fitch from 'AA' because the state maintained much stronger dedicated operating reserves through a challenging budget cycle, indicating a sustained improvement in its operating performance. This upgrade resulted from strong budget controls and discipline and a low long-term liability burden that has declined over time.

New Jersey upgraded by S&P to A+ and Moody’s to Aa3. The upgrades reflect better budgetary operations resulting in surplus and adding to reserves while also reducing large debt and pension liabilities.

Connecticut upgraded by Moody’s to Aa2 and Fitch to AA. The change reflects strong governance practices that have led to increased budgetary reserves and consistent pension contributions that have begun moderating the state's very high unfunded pension liabilities.

Fitch upgraded Alaska to 'AA-', noting the maintenance of robust reserves and changes in the states fiscal structure that meaningfully diversify its revenue structure and that are likely to support steadier operating performance on an ongoing basis.

S&P Upgraded Wyoming to AA+ due to demonstrated active budget monitoring, conservative revenue forecasting, and timely expenditure adjustments. Such adjustments can maintain structural budget balance and very high reserves that provide near-term budgetary flexibility to mitigate potential revenue volatility from fluctuating energy markets or economic downturns.

Arizona’s AA rating outlook was changed to stable from positive by S&P. The stable outlook reflects a continued commitment to structurally balanced operations amid a somewhat softening economic environment and to maintaining reserves at higher levels.

Conclusion

Most rated munis are in better position than they were before the pandemic. Municipalities have gotten better at budgeting and maintaining strong reserves, and more of them are recognizing that pension funding is less expensive in the long run when pensions are adequately funded each year so that the funded level increases.

There are, however, challenges on the horizon for munis, as municipalities confront an array of new and fast-moving developments. The importance of protecting against cyber threats and extreme weather threats has been made all too real to the nation. Further, AI computing and data centers, while bringing us efficiency, growth, and changes in how we approach work, are straining our electricity and water supplies.

At Cumberland Advisors we invest in high-quality munis that have diverse economies and robust financial operations, which give them an average rating of AA. These attributes provide munis with more flexibility to adapt to challenges and opportunities.

Patricia Healy, CFA

SVP, Research

Feedback | Bio

Sign up for our Market Commentaries

Cumberland Advisors Market Commentaries offer insights and analysis on upcoming, important economic issues that potentially impact global financial markets. Our team shares their thinking on global economic developments, market news and other factors that often influence investment opportunities and strategies.

Links to other websites or electronic media controlled or offered by Third-Parties (non-affiliates of Cumberland Advisors) are provided only as a reference and courtesy to our users. Cumberland Advisors has no control over such websites, does not recommend or endorse any opinions, ideas, products, information, or content of such sites, and makes no warranties as to the accuracy, completeness, reliability or suitability of their content. Cumberland Advisors hereby disclaims liability for any information, materials, products or services posted or offered at any of the Third-Party websites. The Third-Party may have a privacy and/or security policy different from that of Cumberland Advisors. Therefore, please refer to the specific privacy and security policies of the Third-Party when accessing their websites.