The end of the second quarter of 2025 saw slight rises in the 10-year Treasury yield but slight lowering of yields in the 10-year AAA muni yield. When you look at the highs and lows for the various maturities of both Tax-exempt munis and US Treasuries you realize the volatility that buffeted both markets.

AAA

| 3/31/2025 | 6/30/2025 | Diff | |

| 2 | 2.75 | 2.59 | -16 |

| 5 | 2.93 | 2.68 | -25 |

| 10 | 3.30 | 3.28 | -2 |

| 30 | 4.28 | 4.54 | +26 |

| HIGH | LOW | ||

| 2 | 3.40 | 2.45 | |

| 5 | 3.59 | 2.59 | |

| 10 | 3.89 | 2.97 | |

| 30 | 4.84 | 3.99 |

TSY

| 3/31/2025 | 6/30/2025 | Diff | |

| 2 | 3.89 | 3.72 | -17 |

| 5 | 3.95 | 3.79 | -16 |

| 10 | 4.21 | 4.23 | +2 |

| 30 | 4.57 | 4.77 | +20 |

| HIGH | LOW | ||

| 2 | 4.05 | 3.61 | |

| 5 | 4.17 | 3.71 | |

| 10 | 4.60 | 3.99 | |

| 30 | 5.09 | 4.41 |

On the Treasury side we had plenty of volatility during the quarter, which came in the form of concern over tariffs (still with us). The market absorbed talk about 50% tariffs for some countries. Eventually, a 90-day moratorium was imposed (expiring July 9th). But in April this sent the bond market reeling between thoughts that tariffs would plunge the country into a recession or result in much higher inflation. Another example of the volatility: In the first full week of April we saw the ten-year Treasury move from a 4.10 to 3.90 almost overnight on fear of a slowdown and then rocket to an intraday high of almost 4.70 during that week on fears that the President would try to remove Jay Powell as Fed chair (he can’t do so, by law, and he backed off from this stance).

The ten-year AAA muni yield, which moved from a 3.26% to 3.20%, was also subjected to a lot of volatility. There was the continued concern (a holdover from first quarter) about the taxation of municipal bonds. We know there were concerns about taxation of munis in three different scenarios. At various times, there was Congressional discussion about taxing munis on forward issuance. Then discussions about taxing existing issuance as well, and finally discussion about imposition of a 28% cap on the benefit of tax exemption. (In other words, if you were in the 35% tax rate, you could only enjoy the benefit of federal tax exemption up to the level as if you were in the 28% bracket.) We always thought these various proposals would fall by the wayside. Our feeling was that in an economy where various federal services seem to be being laid off onto state and local governments, it would be disingenuous of the federal government to take away state and local governments’ ability to finance these services and projects at an advantageous rate. In the end we ended up with the House bill not doing anything on munis, and this was certainly helped by Congressman French Hill of Arkansas, Chair of the House Financial Service Committee, writing to the House Ways and Means Committee, urging them to leave tax-free munis alone, especially in the light of the role they are playing in building and expanding the country’s infrastructure. The market was able to breath a sigh of relief last week when the Senate version of the bill also did not include any taxation of munis.

Munis were also bothered in April by the volatility of Treasuries due to tariffs and Jay Powell talk. This made it impossible for municipal underwriters and dealers to hedge either unsold balances from new deals or secondary blocks they were bidding on. The result of this was new deals being priced extremely cheap and secondary bids being dropped. This volatility lessened as the tariff and Jay Powell talk quieted down. Both Treasuries and munis finished much lower than their early-second-quarter highs in yields.

Once there was some clarity in the muni market, we saw issuance pick up sharply, and supply through the midpoint of the year is running about 32% ahead of 2024’s record. We do think that the pace of issuance should slow down somewhat during the second half of the year. You can see that longer-term bond yields moved up during the quarter in both Treasuries and tax-free munis. We think a lot this was driven by the uncertainties that both markets faced.

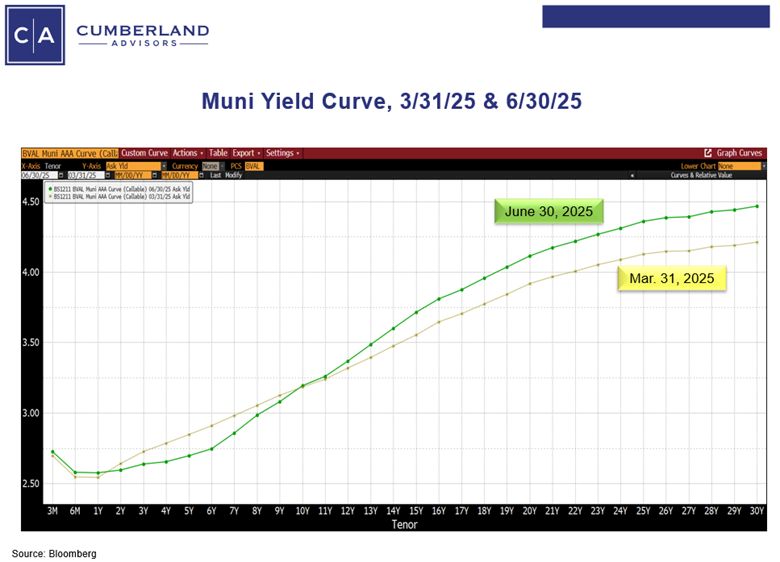

Looking at the AA muni yield curve at the start of the quarter and the end; We can see the overall steeping. We think some of this gets reversed in the second half of the year.

Now that the tax bill has been passed by both the House and the Senate, we think that longer bond yields can come down – particularly in the muni sector. The graphs below shows both the Treasury and AA muni curves at the end of the first quarter and the end of the second. You can clearly see the change in both markets with steepening. We think some of this steepening is reversed in the third quarter due to increased clarity with the tax bill behind us. In particular, longer munis seem very oversold when you look at taxable equivalent yields. The longer, 30-year-plus part of many muni deals are at the 5% level or above. 5% is a 7.93% taxable equivalent on the federal level, and if there are state taxes involved, it moves to over 8% taxable equivalent.

We do believe that the economy is slowing, and though tariff talks are keeping the Federal Reserve on hold for now, we do think that the Fed will most likely be cutting short-term rates later in the year. Last September, the Fed’s first rate cut of 50 basis points saw higher long-term bond rates as you move to the end of the year. We believe that the turnaround in the Trump Presidential campaign and investors’ belief that Trump would (along with a House and Senate on the same side) produce higher inflation expectations and thus a need for higher long-term yields. It’s important to note that since the day after the election, the ten-year Treasury is down about 10 basis points in yield and down from 4.80% the week before the inauguration in January 2025. More importantly, trailing 12-month headline inflation is down to 2.4% from 2.9% at year end. This time when the Fed cuts, longer term rates should follow.

John R. Mousseau, CFA

Vice Chairman | Chief Investment Officer

Email | Bio

Sign up for our Market Commentaries

Cumberland Advisors Market Commentaries offer insights and analysis on upcoming, important economic issues that potentially impact global financial markets. Our team shares their thinking on global economic developments, market news and other factors that often influence investment opportunities and strategies.

Links to other websites or electronic media controlled or offered by Third-Parties (non-affiliates of Cumberland Advisors) are provided only as a reference and courtesy to our users. Cumberland Advisors has no control over such websites, does not recommend or endorse any opinions, ideas, products, information, or content of such sites, and makes no warranties as to the accuracy, completeness, reliability or suitability of their content. Cumberland Advisors hereby disclaims liability for any information, materials, products or services posted or offered at any of the Third-Party websites. The Third-Party may have a privacy and/or security policy different from that of Cumberland Advisors. Therefore, please refer to the specific privacy and security policies of the Third-Party when accessing their websites.