Cumberland has used separately managed accounts (SMAs) to execute its fixed-income strategies since the company’s inception in 1973, long before SMAs were popularized in the early 2000s.

The reasons for managing money in this fashion are the same today as they were then:

Transparency (you know what you own)

Flexibility to make strategic changes

Ability to manage transaction costs and best execution

Active management

SMAs offer individually tailored portfolio management options to address client objectives, including tax management, income production, state-specific taxation exemption, cashflow needs, and client-specific customizations. SMAs differ from pooled vehicles like mutual funds and ETFs in that each portfolio can be designed uniquely to a single investor. SMAs also differ from pooled vehicles in terms of (a) transparency, (b) containing stated maturity dates (c) liquidity management within the portfolio, and (d) flexibility for tax management, such as tax loss harvesting or customized state bias weightings.

Growth in SMAs

The advantages of SMAs have led to their increased use by investors. SMA municipal fixed-income assets, both taxable and tax-exempt, have grown from $100 billion in 2008 to an estimated $1.2 trillion of the $4 trillion market at the end of Q1 2025. SMA municipal assets have increased while direct retail and mutual fund assets have declined. Mutual funds, including money market, closed-end funds, and ETFs totaled $1.14 trillion in muni holdings at the end of Q1 2025. SMA holdings are not separately reported in the Fed data; they are a subset of the household or retail holdings. The Q1 data that we cite is from JPMorgan and was estimated by data derived from SEC Form ADV filings by investment management firms and JPM customer surveys.

Technological improvements have also made it more efficient for managers to offer lower minimums for investing in fixed-income SMAs. At Cumberland our minimum is $250,000 and has been for some time. This size allows us to purchase enough bonds to provide diversification.

ETFs

Exchange-traded fund (ETF) volume has grown almost 73% since 2021 to over $150 billion. Although fast-growing, ETFs constitute only 3% of the $4 trillion municipal market. Conversion of mutual funds to ETFs, as well as organic growth of ETFs, has contributed to the increase. Advantages of ETFs include intraday liquidity, low cost, diversification for smaller investors, and quick exposure to the asset class for larger managers. Some investors have chosen to move into ETFs as a placeholder in anticipation of bigger supply and higher rates, before reinvesting in individual bonds or SMAs.

Fund Flows

Mutual fund flows, followed regularly by the market as an indication of demand, are affected by a herd mentality and thus present opportunities for active fixed-income management. Flows into and out of mutual funds can turn very quickly. When investors are dumping assets, the mutual fund portfolio manager may not be able to fully practice active management and must liquidate funds as required by redemptions. Direct retail and SMAs tend to be stickier and, for example, may be able to take advantage of opportunities/yields when the market gets oversold.

Demand, Muni Bond Volume and Value

The muni market has experienced good demand this year even with the substantial increase in issuance. Issuance has grown from $485 billion in 2021 (having dipped to $385 billion for each of 2022 and 2023) to $508 billion in 2024. Volume for 2025 is already surpassing levels from this time last year; and by some estimates, if issuance keeps on track, volume could be $535 billion. The increase in issuance is due to numerous factors, including municipalities retaining funds to increase reserves for unseen events, funding deferred maintenance, building new infrastructure to maintain resiliency, and accommodating the changes in funding to states and projects that the federal government is considering.

Over the past 20 weeks, there have been 18 weeks of inflows into mutual funds and ETFs – an indication of demand likely reflecting higher muni yields and strong ratios. The 10y muni was at 2.93%, and the 10y Treasury was 4.06% for the week ending September 12, which results in muni/Treasury ratios of 71% for the 10y and 90% on the 30y. Depending on an investor’s tax bracket, these levels provide compelling taxable equivalent yields.

More thoughts on muni portfolio management and muni yields can be found in Ben Pease’ July 9th commentary A Forward-Looking Perspective on Municipal Bonds.

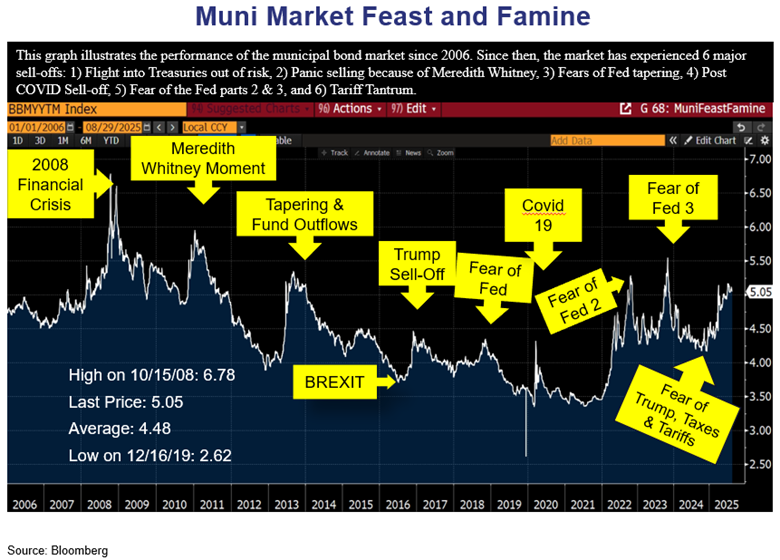

The chart below shows that cycles of inflows and outflows have occurred numerous times, and each time the recovery in rates has been quick.

Municipal Bond Credit Quality

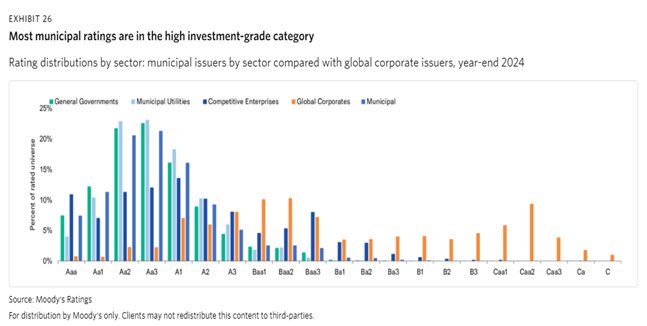

Municipal bonds in general have higher ratings, less correlation to corporate bonds, and higher yields than other worldwide offerings do. Moody’s data show that many muni bonds are rated in the Aa category, while corporate bonds are skewed to the lower ratings, including non-investment-grade and many in the Baa category. At Cumberland we invest in taxable munis in our taxable fixed-income strategies, in addition to Treasurys, agencies, and highly rated corporate bonds.

Efficiencies

At Cumberland we buy bonds in aggregated lots and allocate positions to individual portfolios, a strategy which may allow for better execution and pricing for our clients compared with doing individual trades for each client. When selling for individual-client money-raise requests, we use our extensive network of resources and knowledge of the markets and the particulars of a client’s portfolio to achieve best execution.

Retail accounts do not enjoy the economies of scale that are available to an SMA manager. In addition, active SMA managers that practice total-return investing may have credit-research resources and relationships with many broker dealers that allow them to achieve competitive execution and develop strategies to optimize investment holdings to meet individual clients’ needs.

While mutual fund shares can be purchased and sold any day in any amount, an SMA account has many individual holdings that may take longer to sell. However, when an investor sells shares in a mutual fund, the price received is calculated at the end of the day, based on the net asset value of the fund. If an investor is instead invested in high-quality liquid bonds like the ones Cumberland purchases in its accounts, then, barring an extraordinary event in the market, there should be ample liquidity, and the bonds could be sold at a time achieves best execution. Additionally, knowing our clients’ needs, Cumberland is looking ahead to provide liquidity when needed. SMAs provide the advantage of customization, allowing clients the ability to determine sectors or categories to be excluded or included for a client’s desired impact, such as no tobacco-related securities or an emphasis on education or water quality. Customization is not possible with a mutual fund or an ETF.

Separately managed accounts generally have higher minimum investment requirements than mutual funds, ETFs, and robo advisors do; so they are not available to all investors. But as an investor acquires more assets and develops more highly tailored goals and objectives, an SMA may be appropriate.

Finally, the management fee charged on SMA accounts can be affected by the competitive environment. The fee is based on the type of strategy and can be scaled based on the level of assets invested. There may also be custodial fees charged to the account. Mutual funds have an expense ratio, which includes a management fee as well as miscellaneous ancillary expenses, custodial expenses, and a distribution charge. Many have various levels of sales charges. So, it is important to look at all expenses when comparing funds.

The Cumberland Approach

At Cumberland we have a top-down approach to investment management. We look at global macroeconomic conditions and policies to assess interest rates and growth prospects to position our portfolios accordingly. Each market and/or sector is evaluated as to how it fits into the global outlook as well as how its idiosyncratic elements may affect supply and credit quality.

The majority of our fixed-income portfolios are managed on a total-return basis using a barbell strategy to take advantage of changes in interest-rate and technical movements more quickly. The use of a barbell strategy allows us to invest in various short-term instruments that are liquid and to use them as ammunition to buy longer-dated bonds when interest rates rise or to take advantage of the higher coupons of longer-maturity bonds compared with shorter-dated bonds. Floating-rate notes and inflation-protected securities are investments that can help returns in the face of inflation and rising interest rates.

Returns of an account are measured against a benchmark, which is usually an index that is widely recognized. Outperformance may mean that individual portfolio returns are less negative than the benchmark’s return or that positive returns are greater than the benchmark’s.

Fixed-income total-return investing takes into consideration price appreciation or depreciation and the effects of coupon income generated and reinvested. Coupon payments over time are a large contributor to the return of an account, but the timing of buying and selling and the choice of where along the curve to buy or sell can greatly impact returns. Other buy-sell considerations include duration, or the sensitivity of a bond to changes in interest rates; embedded options such as call features; supply and demand; coupon structure; and credit-quality trends. All of these can affect the performance of a portfolio relative to an index or benchmark. Finally, to quote Cumberland’s CIO John Mousseau, “Active management means active thinking, not always active trading.”

In summary, we continue to operate as Cumberland’s founders did, investing clients’ funds in separately managed accounts. Our approach to investing is top-down and takes account of global interest-rate expectations and credit-quality trends as well as characteristics of each bond.

Patricia Healy, CFA

SVP, Research

Feedback | Bio

Sign up for our Market Commentaries

Cumberland Advisors Market Commentaries offer insights and analysis on upcoming, important economic issues that potentially impact global financial markets. Our team shares their thinking on global economic developments, market news and other factors that often influence investment opportunities and strategies.

Links to other websites or electronic media controlled or offered by Third-Parties (non-affiliates of Cumberland Advisors) are provided only as a reference and courtesy to our users. Cumberland Advisors has no control over such websites, does not recommend or endorse any opinions, ideas, products, information, or content of such sites, and makes no warranties as to the accuracy, completeness, reliability or suitability of their content. Cumberland Advisors hereby disclaims liability for any information, materials, products or services posted or offered at any of the Third-Party websites. The Third-Party may have a privacy and/or security policy different from that of Cumberland Advisors. Therefore, please refer to the specific privacy and security policies of the Third-Party when accessing their websites.