US Stock Market: Point and Counterpoint

Today we want to take a point and counterpoint approach to considering the valuation of the US stock market.

One point of view is that the markets are overvalued. Here’s the “overvalued and vulnerable,” argument from Philippa Dunne in TLRwire. (Readers may subscribe at https://www.tlranalytics.com). We thank Philippa and Doug Henwood of TLR Analytics for permission to share their charts and analysis. TLRwire has long been a must-read publication at Cumberland.

The counterpoint view maintains that the market is, in fact, a bargain; and pricing power is the key factor. Jonathan Golub, Managing Director and Chief U.S. Equity Strategist for Credit Suisse, offers thought-provoking charts and analysis. We thank him for permission to reproduce for our readers his perspective on the markets.

Following these two excellent pieces, which we believe are best considered together, we will offer our own take.

“September 1929, Now an Also-Ran”

TLRwire, September 27, 2021

There are many ways to say the US stock market is insanely overvalued, and here are three graphs making the point. They lead to the sensational projection that the S&P 500 could lose almost half its real value over the next decade.

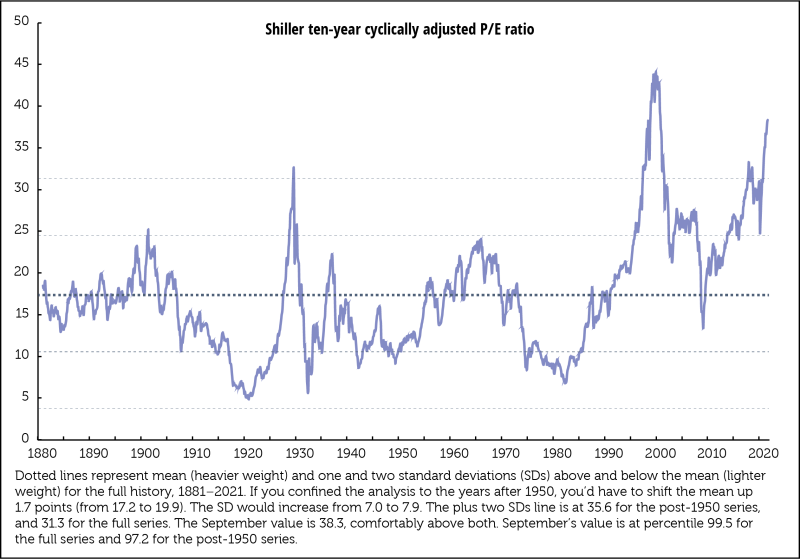

First, valuation, using Robert Shiller’s cyclically adjusted price/earnings (CAPE) ratio, price divided by the ten-year trailing average of real earnings. September 2021’s reading, 38.3, is surpassed only by April 1999’s 42.7. September 1929 looks like an also-ran, at 32.6.

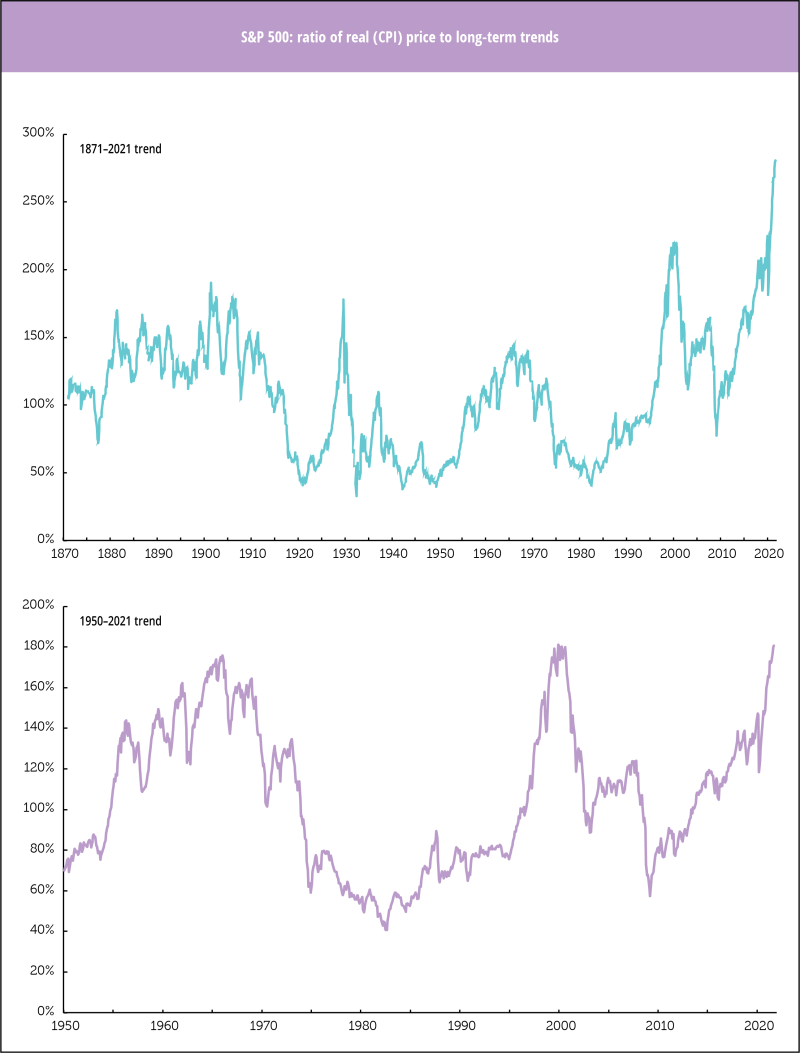

And now the ratio of actual price to the long-term trends in real prices, both for the full sample (1871–2021) and for the years after 1950. For the full series, September’s reading of 281% leaves July 1999’s 216% and September 1929’s 178% in the dust. For the post-1950s series, September’s 181% ties December 1999’s reading and beats December 1966’s 176%. The highs of 1929 and 1999/2000 need no further comment; both preceded sharp drops in the market, 81% from 1929 to July 1932, and 45% from April 2000 to October 2002 (both in real terms). The 1966 high in the ratio came in ahead of the eventual high in the real S&P, 299.1 in December 1968. After that high, the real value of the S&P went alternately sideways and down until eventually bottoming out in July 1982, with a loss of 54% in real terms. It wouldn’t surpass that 1968 peak in real terms until January 1992, over 23 years later.

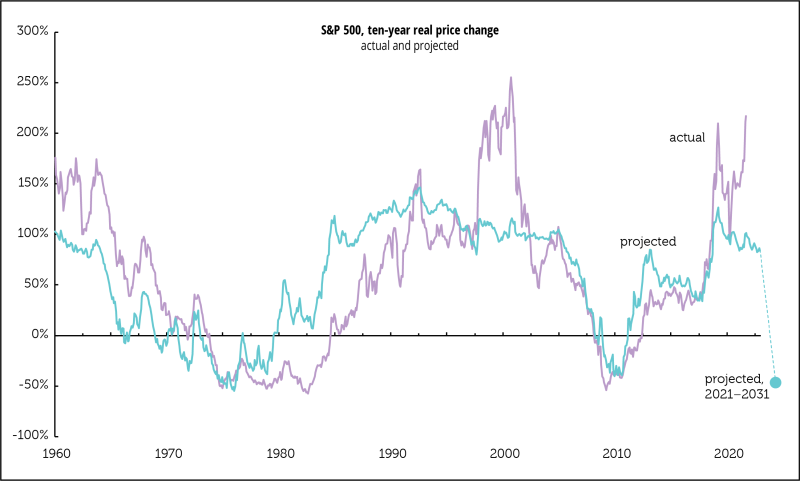

And, finally, putting these two valuation measures together to produce a long-term forecast. For this exercise we’re using only the post-1950 history, because the high current valuations produced by the full history produce a nonsensical projection of over a 100% loss. Graphed below is a ten-year-ahead prediction of future prices based on the values of Shiller’s CAPE and the actual/trend real price ratio. The projection in the graph is shifted ahead by ten years to match the model with the outturn. For a long-term forecast, it looks pretty good. Two points: we don’t really “deserve” today’s high prices. By this crystal balling, prices “should” be less than half what they are. And the other: the future doesn’t look like one so bright that it would cause the historically inclined reader to don shades—a real decline of 46%. As outlandish as that might seem, the model was pretty on-target for the declines into the mid-1970s and again into 2010.

Now that the Fed and other central banks are turning away from years of pumping out free money, it will be very interesting to see if this model gets things right again.

—Philippa Dunne & Doug Henwood

Let’s get to the opposite viewpoint.

“EBIT margins approaching all-time highs”

Jonathan Golub

Email, September 29, 2021

Yesterday’s note (Pricing Power + Operating Leverage: Industrials vs Tech) highlighted—via a hypothetical example—how margins for Cyclical companies benefit more from inflation and operating leverage than their Tech peers. Today’s note shows how this is playing out empirically.

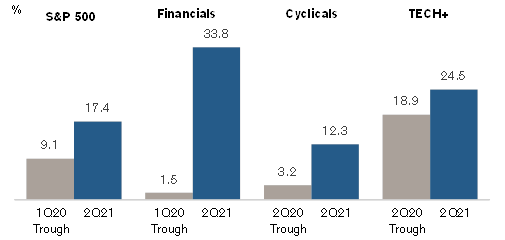

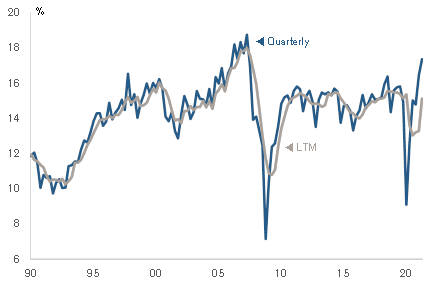

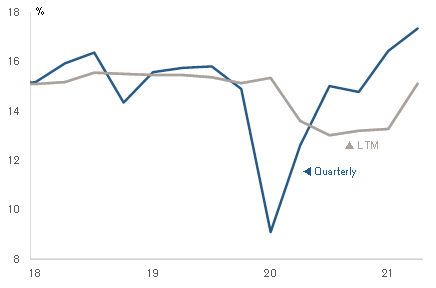

S&P 500 EBIT margins have jumped 91% from their pandemic lows (9.1% to 17.4%), surpassing prior-cycle peak levels (16.4%). That said, they remain below their all-time peak in 2007 (18.8%), representing further potential upside, in our opinion.

All sectors have witnessed improvement in their EBIT margins; however, Financials and Cyclicals have experienced larger increases than TECH+ and Non-Cyclicals.

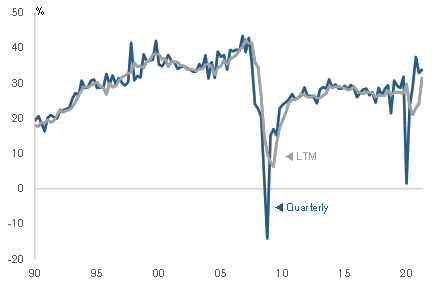

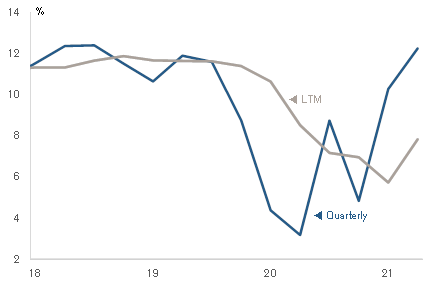

■ Financial margins collapsed at the onset of the pandemic on large loan loss reserves. Strong trading and banking activity, along with the reserve releases, have contributed to the group’s outsized rebound.

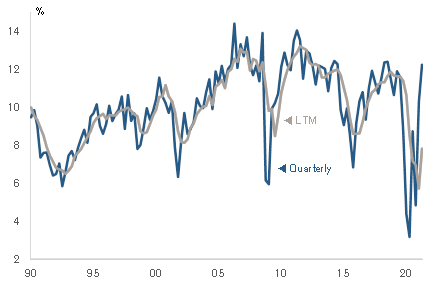

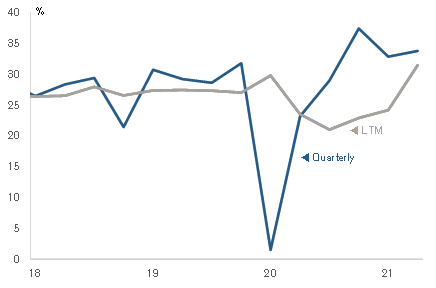

■ Cyclicals saw their margins collapse from 12.4% pre-COVID to 3.2% in 2Q20, and have subsequently jumped ~300% on strong pricing power and operating leverage. They currently sit roughly in-line with pre-crisis levels. More economically-sensitive companies with large fixed overhead should see even further upside.

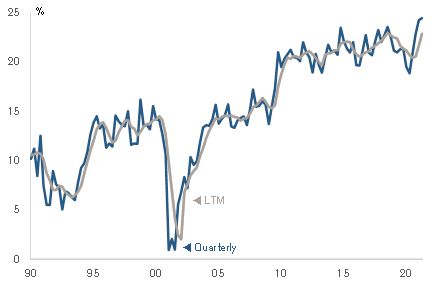

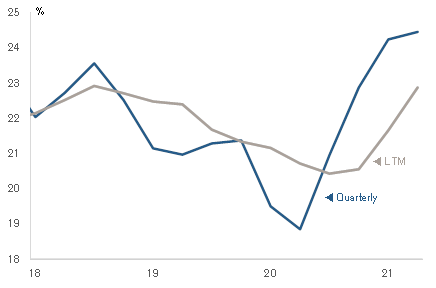

■ TECH+ EBIT margins fell more modestly during the pandemic (23.6% to 18.9%), and currently sit at all-time highs (24.5%). We believe margin upside will be more limited for TECH+ companies given their lack of operating leverage.

EBIT Margins: Recent Trough vs. Latest Quarter

EBIT Margins Long-term Trends: S&P 500

EBIT Margins Long-term Trends: FINANCIALS

EBIT Margins Long-term Trends: CYCLICALS

EBIT Margins Long-term Trends: TECH+

EBIT Margins Near-term Trends: S&P 500

EBIT Margins Near-term Trends: FINANCIALS

EBIT Margins Near-term Trends: CYCLICALS

EBIT Margins Near-term Trends: TECH+

Jonathan Golub, CFA

Chief U.S. Equity Strategist

& Head of Quantitative Research

Credit Suisse Securities (USA) LLC

We thank Philippa Dunne and Jon Golub for sharing their views of market valuation. Let’s add our view.

First, we believe it is important to read and research all points of view. The worst thing is to read or listen to viewpoints that are only consistent with your own. All that does is reinforce your own mistakes.

If I had to choose a single research piece to read, I would prefer something that challenged my view or disagreed with me. Note that in all cases we prefer the argument be curated and supported with data. That doesn’t make if the “right” argument but it does give a reader the benefit of seeing the assumptions and rationale behind a forecast or view point. People who just “wing it” with an opinion or trolls who hide behind some anonymous social media site don’t help the decision making process. But an argument with citations that makes you pause and consider it, is worth reading.

We believe both of these stock market valuation arguments have merit. They approach the market from differing platforms. Our view has a worrying component because of the slowing of the economy. And we have repeatedly argued that a pandemic shock is not a usual or normal business cycle. Lastly, we do not believe the COVID pandemic is over. And we are only just beginning to absorb the size of the Long COVID health shock and how much of it impacts the labor force.

So these negative elements would support the TLR view of an excessive and highly priced stock market.

But there is another component which occurs following pandemics. Wages rise because there are fewer people to do the work. Businesses then reallocate resources from the labor component to the capital component. When they do an investment results and the business obtains a productivity gain. Thus the remaining labor force earns more income and the businesses are more productive and the return on certain capital investment is enhanced. This outcome would support the Jon Golub view.

Lastly, we are money managers so that means what we do is the most important thing. Research services and opinions are important but, at the end of the day, the money manager has to decide to buy, sell or hold.

Presently, we have some cash reserve which we may deploy at any time. The cross currents in the market may present us with a pullback and entry opportunity. We’re watching the mess in Washington and the destructive political divide in the country. And were watching what the Fed will do and when they will do it. Lastly, we continue to favor the healthcare sector even though it is has been flat for a while. Meanwhile, the quantitative component in our stock ETF portfolios is on the offense with two recent buy signals. So that outcome means in the quantitative portions of portfolios, we are fully invested in the 4 different Quantitative Strategies and we favor the higher beta sectors.

Of course, these portfolios may change at any time and without any notice except to clients who are able to access their portfolios daily.

We hoped readers enjoyed the point and counter point.

David R. Kotok

Chairman of the Board & Chief Investment Officer

Email | Bio

Links to other websites or electronic media controlled or offered by Third-Parties (non-affiliates of Cumberland Advisors) are provided only as a reference and courtesy to our users. Cumberland Advisors has no control over such websites, does not recommend or endorse any opinions, ideas, products, information, or content of such sites, and makes no warranties as to the accuracy, completeness, reliability or suitability of their content. Cumberland Advisors hereby disclaims liability for any information, materials, products or services posted or offered at any of the Third-Party websites. The Third-Party may have a privacy and/or security policy different from that of Cumberland Advisors. Therefore, please refer to the specific privacy and security policies of the Third-Party when accessing their websites.

Cumberland Advisors Market Commentaries offer insights and analysis on upcoming, important economic issues that potentially impact global financial markets. Our team shares their thinking on global economic developments, market news and other factors that often influence investment opportunities and strategies.