The opening of the April 27th Economist article about the dollar started with this:

Every so often an appetite surges for an alternative reserve currency to the dollar—and a market booms in predictions of the greenback’s imminent demise. For nearly three-quarters of a century the dollar has dominated trade, finance, and the rainy-day reserve portfolios of central banks. Yet high inflation, fractious geopolitics and the sanctions imposed by America and its allies on countries such as Russia have lately caused dollar-doubters to become vocal once again.

(“The power and the limits of the American dollar,”

https://www.economist.com/leaders/2023/04/27/the-power-and-the-limits-of-the-american-dollar)

Let’s discuss our view on the dollar; but before we do, we want to share a little story.

Many years ago, there was an employment ad in the Wall Street Journal. A major bank was looking for an experienced currency trader. Dmitri (fictional name intentionally) applied for the job. On his extensive résumé, he listed positions as head currency trader in three previous institutions.

Here’s the part of his history that was not listed in the résumé.

Dmitri traded the D-Mark versus the US dollar at the first institution and had some successes, making a few million for bank #1. Then, in a crisis, he missed trades and ended up losing 50 million of the bank’s money. The bank never recovered and eventually merged. And Dmitri was in search of his next job.

When hired by the second bank, Dmitri listed his expertise as specializing in trading European currencies versus the dollar. Bank #2 gave him some limited lines, and he again traded successfully for several months. Management kept enlarging the lines as time went by. And then the unexpected happened again. The markets were jolted by a shock, and Dmitri lost large sums for the bank’s trading accounts. Again, the trade that sank him was D-Mark-USD. That bank, too, was subsequently merged, and Dmitri was job hunting again.

His third currency trading job came a few years later, during the launch of the euro after the final terms of the Maastricht Treaty were set. For the three years of the virtual launching period, the individual-country currencies were still trading, and formula linkages to the new euro were applied. Dmitri took a strong euro stance in very large sums of bank’s money, and he used the D-Mark versus the dollar as the actual trade. However, the euro continued to weaken during the entire three-year period, which meant that all his bets on a strong D-mark were going against him. The expected outcome slammed his employer bank.

Fast-forward to the interview for his next job.

With his résumé listing all the prior positions held with the pre-merger institutions, Dmitri made it to the top of the short list. In the final interview, the HR chief professional advised Dmitri that they were looking for a seasoned trader to handle the US dollar-yen book. Dmitri said “No.” When asked why, he replied, “I’m not qualified to trade dollar-yen for you.”

HR wondered, “You have all this experience on your resume — why don’t you qualify?”

Dimitri responded, “Because I’m an expert in D-Mark-dollar and not in dollar-yen.”

In my opinion, the risks to successful shorter-term currency trading are about equal to the rewards after one adjusts for the hedging costs. That doesn’t mean a person cannot successfully trade FX. Some do. And some, like Dmitri, do it for years and then get slammed. For those doubters of this story, let me just say that my first experience with the D-Mark was when it traded at a ratio of 7:1 against the US dollar. I personally watched the market change to 4.2:1. I was in Germany at the time.

Hedged FX trading is done by a large pool of professionals who are active all the time, around the world. They represent the economic and financial institutions who are engaged in global finance. They assist their respective employers who are either selling or buying in two different currencies or more than two. And they help in the global financing that uses interest-rate swaps and cross-currency swaps. Those professionals try to dampen risk, and they drive daily market prices of many instruments.

Enter the speculator in FX.

She or he tries to outguess the market. There are many approaches and a diverse set of tools. Examples: Does one use purchasing power parity, or current account deficits or surpluses, or comparative real interest rates, or movements in gold prices, or disparities in central bank’s balance sheets, or reliability of various legal systems, or political stability and war risk, or probabilities of mean reversion versus tail risks? Does trading momentum help? Are there quantitative strategies that can work successfully over a longer period? And what is an appropriate period to evaluate these results? Are speculators better off doing day trades based on intraday momentum?

Opposing the speculator is the professional described above. Here are two examples from among Cumberland’s clients.

A real estate developer uses interest-rate swaps in all his financing in order to determine the true cost of finance. He negotiates them with his bank. That bank is constantly hedging the other side of the risk in the swaps market. Many of those transactions become cross-currency interest-rate swaps, and that occurs whenever the market pricing of the FX rate provides a cheaper outcome for the intermediary bank or for the client or for both. This activity is constant and in the trillions worldwide. Thus, the developer-borrower may not even know his transaction is linked in a chain to another currency. And he doesn’t really care, as long as he gets the financing structure that matches his risk and maturity needs.

Example two. A large medical facility is buying an expensive equipment installation made in Europe. The price is set in euros, and the terms are for a delivery in two years. The buyer is American and budgets in US dollars; the seller operates in euros. The foreign exchange risk is hedged for both parties in the futures markets. The differential interest-rate risk is also hedged. Thus, the buyer can know exactly what he will pay for the total installation, and the seller can know exactly what to expect in receipts and when to expect them. This is a commercial transaction of a type the occurs in the billions every day.

So where does the US dollar fall in this entire scheme of things?

Michael Cembalest of J.P. Morgan reported in the April 26, 2023, episode of Eye on the Market, “The US share of global trade is just ~12% and the US share of global GDP is ~25%.” Kotok note: US GDP is heavily weighted in services; in goods only, China is larger than the US. So, if US GDP is 25% of world GDP, why is the US dollar about 89% of global FX transactions and 85% of the currency and forward-swap markets? Add to the list 65% of global loan issuance and 88% of international debt issuance. Over half of global invoicing is in US dollars. Sure, the dollar is down to about 60% of world reserve-currency holdings since 2015, and the decline in reserve status is about 6%. But where was the shift? About ¾ of it went into smaller currencies like the Australian and Canadian dollars, Swedish krona, and South Korean won. (See Michael Cembalest, “Oh the Places We Will Go,” J.P. Morgan, https://assets.jpmprivatebank.com/content/dam/jpm-wm-aem/global/pb/en/insights/eye-on-the-market/oh-the-places-we-could-go.pdf?cta=body.)

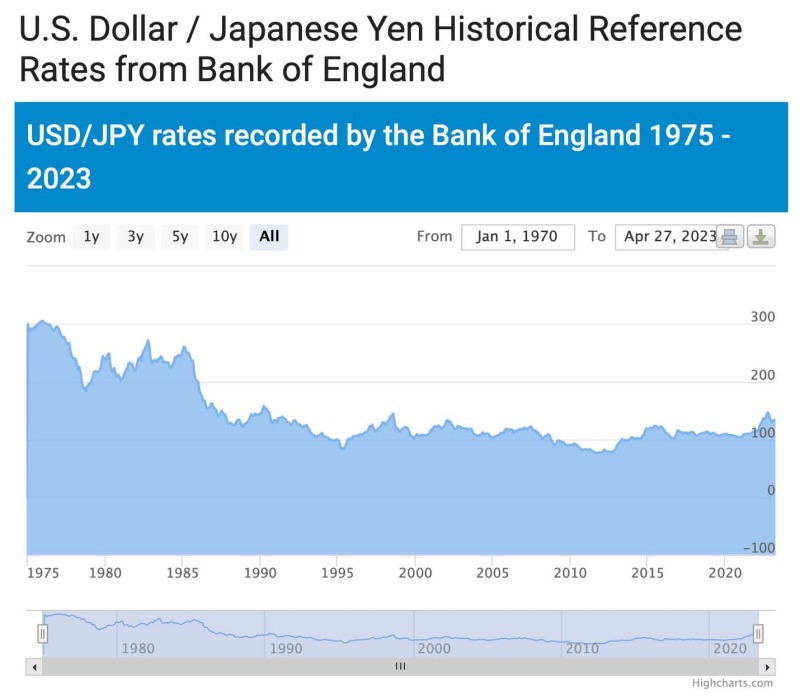

We will skip the euro, which is the second largest reserve holding, and go to the yen. The history (since 1975) of the dollar-yen FX rate is charted below.

(Source: PoundSterling Live, https://www.poundsterlinglive.com/bank-of-england-spot/historical-spot-exchange-rates/usd/USD-to-JPY-1970)

Think about all the factors (some were listed above) that occurred in this period with the yen. Did differential interest rates create this history? Japanese rates have been near zero for decades. Was it inflation rates? Japan hasn’t had inflation for many years. Is it deficits? Nope, theirs are much larger than ours or others. Was it central bank money creation? Not according to the evidence, since in the case of Japan the central bank holds over 100% of the GDP on its balance sheet. For contrast, consider that achieving the same ratio in the United States would require the Federal Reserve to buy nearly all available outstanding US Treasury bills, notes, and bonds. So, why hasn’t the yen collapsed, as many have predicted for decades?

Here’s the history of the US dollar over the last decade and since the impacts of the Great Financial Crisis (2007–2009) subsided.

(“United States Dollar,” https://tradingeconomics.com/united-states/currency)

So, does this history reflect US labor shortages as a result of Covid? The data would say no. Is it US inflation? Where was the inflation two years ago? Is it our rule of law? Maybe. Is it our political stability? Maybe. Is it fear of the debt ceiling fight? Who knows for sure?

Here’s our final takeaway.

At Cumberland, we manage a few billion for others. We don’t trade FX. We stay with US dollar-denominated investments only. And only those regulated within the US legal system.

And, by the way, Dmitri doesn’t work for us.

Links to other websites or electronic media controlled or offered by Third-Parties (non-affiliates of Cumberland Advisors) are provided only as a reference and courtesy to our users. Cumberland Advisors has no control over such websites, does not recommend or endorse any opinions, ideas, products, information, or content of such sites, and makes no warranties as to the accuracy, completeness, reliability or suitability of their content. Cumberland Advisors hereby disclaims liability for any information, materials, products or services posted or offered at any of the Third-Party websites. The Third-Party may have a privacy and/or security policy different from that of Cumberland Advisors. Therefore, please refer to the specific privacy and security policies of the Third-Party when accessing their websites.

Sign up for our FREE Cumberland Market Commentaries

Cumberland Advisors Market Commentaries offer insights and analysis on upcoming, important economic issues that potentially impact global financial markets. Our team shares their thinking on global economic developments, market news and other factors that often influence investment opportunities and strategies.