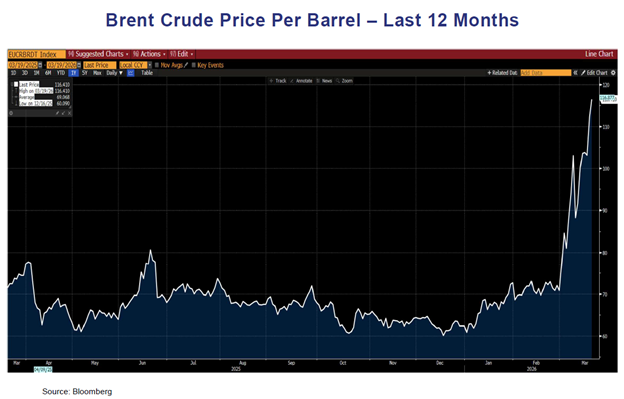

The war against Iran began its fourth week this Sunday. We have seen bond yields rise in both taxable and tax-free bond markets, reflecting mostly the rise in the cost of oil due to shipping stoppages through the Strait of Hormuz. Below is a graph of the price of oil over the last year, and you can see the jump from roughly $70/barrel spiking to over $115/barrel, a 65% increase.

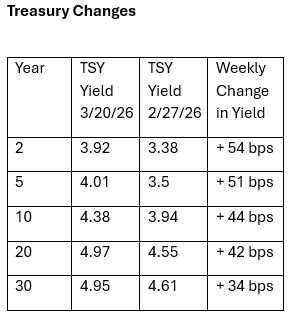

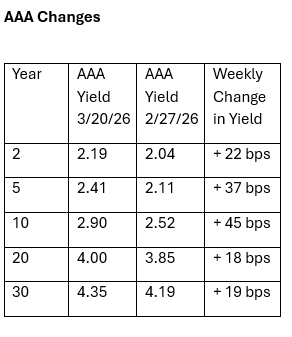

Below is a table showing the changes in yield in both the Treasury market and AAA municipal bonds.

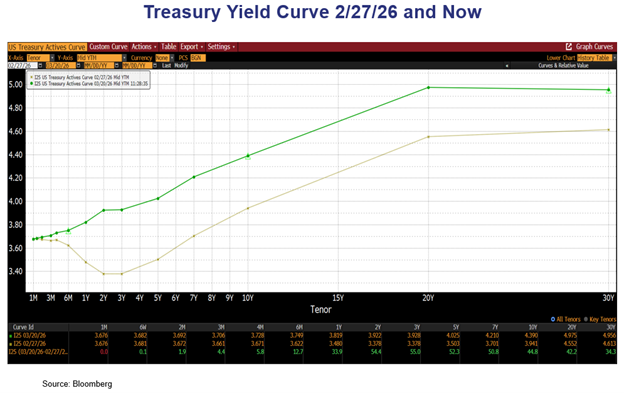

Here is a graph showing the US Treasury yield curve right before the hostilities and now.

Some observations. While all yields are higher, short-term yields have risen more than longer-term yields. Two-year Treasury bond yields are about 55 basis points higher, while ten-year yields are approximately 45 basis points higher.

The factors weighing on the bond market prior to the war were concerns about AI’s impacts on software companies and service companies and the fallout being seen in private credit, all of which was taking bond yields lower, and indeed ten-year Treasury bond yields to levels below 4%. All of that has been changed by the war and concern over the oil not being shipped through the Strait of Hormuz.

The Federal Reserve went out of their way on Wednesday to disabuse investors thinking that there would be any short-term rate cuts in the future. The market has gone from projecting cuts to projecting possible short-term rate hikes in the next year.

Clearly, this trajectory will depend on the duration of the conflict in general and the closure of the Strait of Hormuz in particular. As soon as we have a week of unencumbered passage through the Strait, we think bond yields start to decline. It may take awhile for them to decline, as the markets will want to see how much the price action from the oil shock works its way through various parts of the inflation outlook, e.g., airline costs, labor, goods with oil inputs, etc. But we do think yields will decline.

The bond markets also think the effects of these hostilities will be short-lived rather than long-lived (for now.)

Below we have the two-year and the five-year breakeven yields. These represent a forward measure of inflation expectations by subtracting the REAL yield on an inflation-indexed Treasury from the yield on a nominal Treasury of the same maturity. That is only one measure of inflation expectations, but it is market-derived. We can see that the breakeven inflation rate on the two-year has risen from 2.30% to 3.40% in almost four weeks, while the breakeven inflation rate on the five-year has risen from 2.25% to 2.73%, a rise of 48 basis points.

The bond market is telling us (for now) that the inflation expectations are more contained going out further than in the near term, and the effects are expected to be more near-term than longer-term. The differential between the two breakeven rates has gone from a 5-basis-point difference before the war to over 70 basis points now, reflecting this.

On the muni side there has clearly been a rise in yields as well – again, more in the shorter term than the longer term. There has been good demand for deals this week, and municipal bond funds and ETFs saw inflows of $1.8 billion this week. Most of these are longer-term funds. This has been a very consistent year of inflows into munis, and we think part of this inflow has been some de-risking that we were witnessing even prior to the war in Iran.

Going forward, we will be watching both markets, but the uncertainty in Iran has presented higher yields in the bond market, with long-term expectations of inflation LOWER than short-term expectations are. We will clearly know more as we get some stability in the Strait of Hormuz.

John R. Mousseau, CFA

Executive Vice President | Chief Investment Officer

Feedback | Bio

Sign up for our Market Commentaries

Cumberland Advisors Market Commentaries offer insights and analysis on upcoming, important economic issues that potentially impact global financial markets. Our team shares their thinking on global economic developments, market news and other factors that often influence investment opportunities and strategies.

Links to other websites or electronic media controlled or offered by Third-Parties (non-affiliates of Cumberland Advisors) are provided only as a reference and courtesy to our users. Cumberland Advisors has no control over such websites, does not recommend or endorse any opinions, ideas, products, information, or content of such sites, and makes no warranties as to the accuracy, completeness, reliability or suitability of their content. Cumberland Advisors hereby disclaims liability for any information, materials, products or services posted or offered at any of the Third-Party websites. The Third-Party may have a privacy and/or security policy different from that of Cumberland Advisors. Therefore, please refer to the specific privacy and security policies of the Third-Party when accessing their websites.